At a minimum, lenders will total up all the monthly debt payments you’ll be making for the next 10 months or longer. Sometimes they will even include debts you’re only paying for a few more months if those payments significantly affect how much monthly mortgage payment you can afford. Make sure your mortgage payment (principal, interest, property taxes and homeowners insurance) is no more than 29% of your gross monthly income.

Flood Insurance

An FHA loan is a mortgage loan that is issued by banks and other commercial lenders but guaranteed by the FHA against a borrower’s default. The question isn't how much you could borrow but how much you should borrow. These home affordability calculator results are based on your debt-to-income ratio (DTI). Industry standards suggest your total debt should be 36% of your income and your monthly mortgage payment should be 28% of your gross monthly income. If you are taking out a conventional loan and you put down less than 20%, private mortgage insurance will take up part of your monthly budget.

How much money will be required at closing?

Federal Housing Agency mortgages are available to homebuyers with credit scores of 500 or more and can help you get into a home with less money down. If your credit score is below 580, you'll need to put down 10 percent of the purchase price. If your score is 580 or higher, you could put down as little as 3.5 percent. In most areas in 2023, an FHA loan cannot exceed $472,030 for a single-family home.

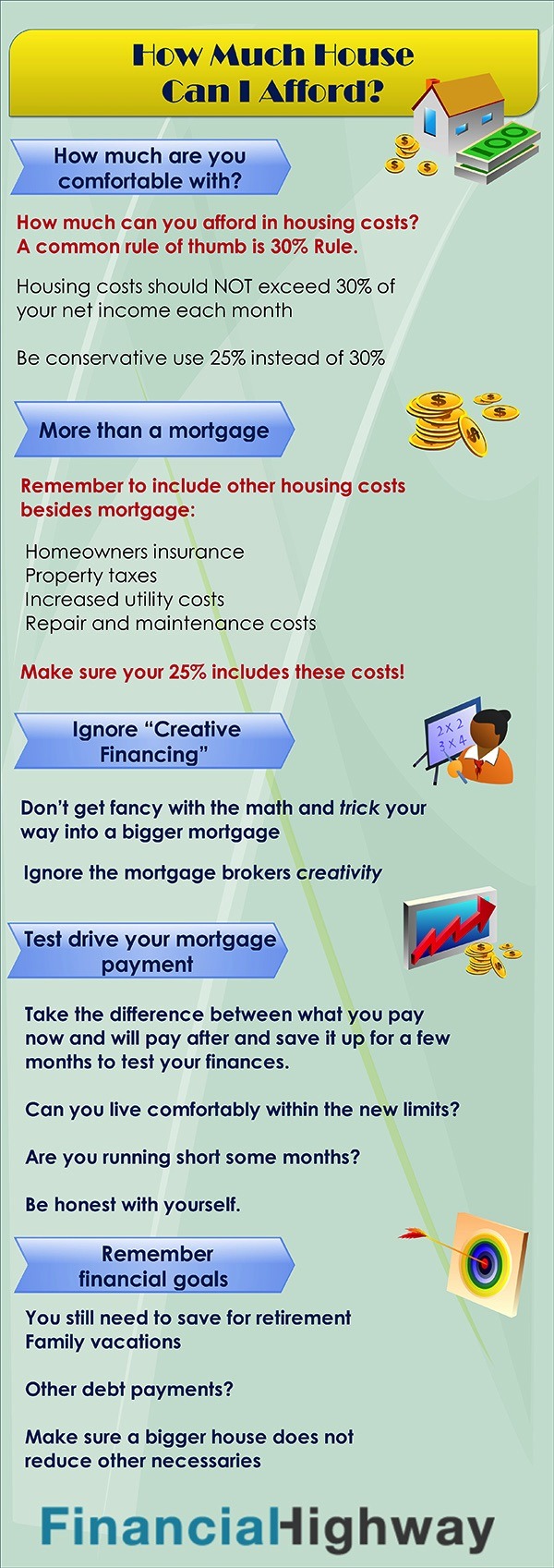

What is a good income to buy a house?

Non-conforming loans are any loans not bought by these housing agencies that don't follow the terms and conditions laid out by these agencies, but are generally still considered conventional loans. A jumbo loan is used when the mortgage exceeds the limit for Fannie Mae and Freddie Mac, the government-sponsored enterprises that buy loans from banks. Jumbo loans can be beneficial for buyers looking to finance luxury homes or homes in areas with higher median sale prices. However, interest rates on jumbo loans are much higher because lenders don't have the assurance that Fannie or Freddie will guarantee the purchase of the loans. USDA loans require no down payment, and there is no limit on the purchase price.

Under "Home price," enter the price (if you're buying) or the current value (if you're refinancing). In order to receive a helpful estimate, it’s important that you input accurate information. Standard conditions include our receipt of homeowner's insurance policy, flood insurance if necessary, and an acceptable title insurance binder. You can also connect with a home mortgage consultant and have a conversation – about your home financing needs, your loan choices, and how much you may be able to borrow.

VA Loan Calculator: Estimate VA Mortgage Payments - NerdWallet

VA Loan Calculator: Estimate VA Mortgage Payments.

Posted: Mon, 26 Feb 2024 08:00:00 GMT [source]

A 5-year ARM, for instance, offers a fixed interest rate for 5 years and then adjusts each year for the remaining length of the loan. Typically the first fixed period offers a low rate, making it beneficial if you plan to refinance or move before the first rate adjustment. We’ll check your credit history to give you an even more solid estimate of what you can afford, along with your expected rate and monthly payment. Generally, the higher the credit score you have, the lower the interest rate you’ll qualify for and improve overall what you can afford in a home. Even lowering your interest rate by half a percent can save you thousands of dollars and increase your affordability range significantly.

If you have excellent credit with a 20% down payment, a conventional loan may be a great option, as it usually offers lower interest rates without private mortgage insurance (PMI). You can still obtain a conventional loan with less than a 20% down payment, but PMI will be required. As a home buyer, you’ll want to have a certain level of comfort in understanding your monthly mortgage payments.

Your credit score largely determines the mortgage rate you’ll get. Even a small difference in interest rate could mean a difference of hundreds or even thousands of dollars in interest you’ll pay over the life of the loan. Interest rates also affect the size of your monthly payment, which has the most direct impact on affordability. However, just because you’re approved for a certain amount doesn’t mean you should buy a house with that home price. Instead, you’ll want to take a close look at your financial health, including your household income and monthly expenses, and make sure to set a firm budget once you begin your home search. But, think of it this way, you’ll improve your chances for a favorable mortgage, which is usually 30 years of your life.

Here's how much you need to earn to afford a Seattle-area home - The Seattle Times

Here's how much you need to earn to afford a Seattle-area home.

Posted: Thu, 29 Feb 2024 08:00:00 GMT [source]

Having an emergency fund can be a good safety net for anyone, especially new home buyers. At a minimum, it’s a good idea to be able to make three months’ worth of housing payments out of your reserve, but something like six months would be even better. That way, if you experience a loss of income and need to find a new job, or if you decide to sell your house, you have plenty of time to do so without missing any payments. Most lenders want you to have a credit score of at least 620 to get a conventional loan. However, it is possible to get a mortgage with a bad credit score, but you will have to put more money down or pay a higher interest rate. A key factor in whether or not you can afford a home is based on the mortgage rate offered.

Our experts have been helping you master your money for over four decades. We continually strive to provide consumers with the expert advice and tools needed to succeed throughout life’s financial journey. Bankrate follows a strict editorial policy, so you can trust that we’re putting your interests first. You’ll have a comfortable cushion to cover things like food, entertainment and vacations. Our partners cannot pay us to guarantee favorable reviews of their products or services.

Your loan program can affect your interest rate and total monthly payments. Choose from 30-year fixed, 15-year fixed, and 5-year ARM loan scenarios in the calculator to see examples of how different loan terms mean different monthly payments. The front-end debt ratio is also known as the mortgage-to-income ratio and is computed by dividing total monthly housing costs by monthly gross income. The Veterans Affairs Department (VA) is an agency of the U.S. government. VA loans make home ownership more possible for borrowers than it otherwise would be through conventional mortgage loans, primarily because a VA loan does not require any down payment.

Naturally, the lower your interest rate, the lower your monthly payment will be. In summary, Los Angeles, CA, is a city with a rich history, diverse geography, and a dynamic economy. It's a place where the entertainment industry meets technology, fashion, and more. The city's political landscape is predominantly Democratic, reflecting its diverse populace. Life in Los Angeles is full of opportunities to explore cultures, cuisines, and outdoor activities, but new residents should be prepared for higher living costs and traffic. Understanding and embracing the unique aspects of Los Angeles can make living in the city a truly rewarding experience.

Most banks don’t like to make loans to borrowers with higher than a 43% debt-to-income ratio. Although it’s possible to find lenders willing to do so (but often at higher interest rates), the thinking behind the rule is instructive. If your mortgage loan is backed by the Federal Housing Administration (FHA), you’ll have the added expense of up-front mortgage insurance and monthly mortgage insurance premiums.

A key step in figuring out how much you’re able to spend on a home is applying for a mortgage. Start the mortgage application process with Rocket Mortgage today. Here are answers to a few frequently asked questions about calculating home affordability so you can better understand your buying power. Next up are several factors that can help you figure out the right price range before you hit the pavement looking for a new home. Another key number in answering the question of how much home you can afford is your down payment. Under "Loan term," click the plus and minus signs to adjust the length of the mortgage in years.

Here are a few documents you should gather to help you understand your financial situation and how much house you can afford. This information will also be required when you apply for a pre-approved home loan. The longer you can stay in a home, the easier it is to justify the expenses of closing costs and moving all your belongings — and the more equity you’ll be able to build.

No comments:

Post a Comment